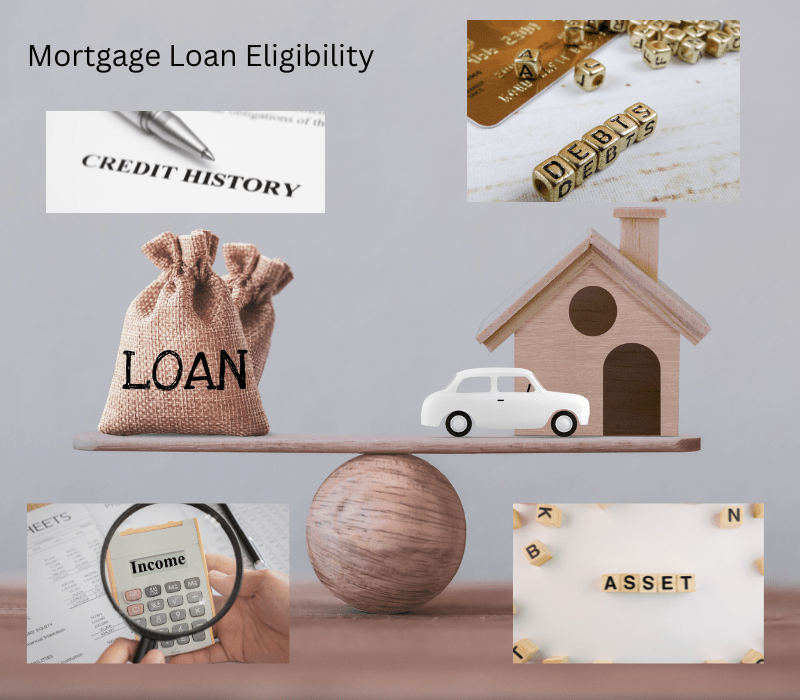

What Determines Mortgage Loan Eligibility is a question to ponder when you start the process of investigating what, how, and how much loan you can or cannot afford.

Buying a home is a big decision, and one of the most important elements to consider is whether you qualify for a mortgage loan. Lenders use a variety of factors to determine your eligibility, including your credit score, income, debt-to-income ratio, employment history, and down payment. Understanding these factors can help you determine if you’re ready to take the next step toward homeownership.

Credit Score and History are the First Determination of Mortgage Loan Eligibility

Your credit score and history are two of the most important factors that lenders consider when determining your mortgage loan eligibility. Your credit score is a numerical representation of your creditworthiness, and it’s based on factors like your payment history, credit utilization, length of credit history, and types of credit.

Lenders typically require a minimum credit score of 620, but a higher score can help you qualify for better interest rates and loan terms. Additionally, lenders will review your credit history to look for any red flags, such as missed payments or collections, that could indicate a higher risk of default.

Income and Employment History

Another key factor that lenders consider when determining your mortgage loan eligibility is your income and employment history. Lenders want to ensure that you have a stable source of income and that you can afford to make your mortgage payments.

The lender will review your employment history to see how long you have been with your current employer and whether you have a steady income. They will also look at your debt-to-income ratio, which is the amount of debt you have compared to your income. Generally, lenders prefer a debt-to-income ratio of 43% or lower.

Debt-to-Income Ratio

Your debt-to-income ratio is one of the key factors that lenders consider when determining your mortgage loan eligibility. This ratio is calculated by dividing your monthly debt obligations by your monthly gross income. Lenders prefer a debt-to-income ratio of 43% or lower, meaning that your monthly debt payments should not exceed 43% of your monthly gross income.

In some instances, when the loan is input into the automated underwriting system, if your credit score is very good (no late payments), your assets are sufficiently verified, and all other criteria are within guidelines, a higher debt-to-income ratio may be allowed. It depends upon the entire underwritten information submitted.

Down Payment and Savings

Another important factor that lenders consider when determining your mortgage loan eligibility is your down payment and savings. Lenders typically require a down payment of 3, 5, 10, or 20 % of the home’s purchase price, depending on the amount of down payment you want to pay.

This also depends on the product type of the mortgage loan you are applying for.

The more money you can put down, the better your chances of getting approved for a loan. Additionally, lenders will also look at your savings to ensure that you have enough money to cover closing costs and other expenses associated with buying a home. It’s important to have a solid savings plan in place before applying for a mortgage loan.

Property Appraisal and Loan-to-Value Ratio

The property appraisal and loan-to-value (LTV) ratio are also important factors that lenders consider when determining your mortgage loan eligibility. The property appraisal is an assessment of the value of the property you want to buy, and it helps the lender determine how much they are willing to lend you.

The LTV ratio is the amount of the loan compared to the appraised value of the property. Lenders typically prefer a lower LTV ratio, as it indicates that you have more equity in the property and are less likely to default on the loan.

Summary

Other factors can come into play, and everything you submit regarding the above is evaluated. This is just the beginning of what mortgage lenders will be looking at initially. However, when reviewing your documentation, there may be additional information requested.

Please note that some lenders have a few standards of their choosing and criteria they want to verify and approve. However, most lenders use the rules of the GSEs, Fannie Mae and Freddie Mac.

We will dive into each of these soon.