Create a Budget…And Limit Your Spending is a simple plan to follow, and we are here to provide some information just for you.

Creating a budget becomes especially important when money feels tight. Whether you’re facing rising expenses, dealing with an unexpected setback, or simply trying to stretch each paycheck a little further, a clear spending plan can help you regain control. Budgeting is not about restriction; it’s about direction.

It gives you a way to prioritize what matters most, reduce financial stress, and make confident decisions even when your income is limited. With the right approach, you can build stability one step at a time and create a spending plan that truly supports your life and goals.

When money feels tight, budgeting isn’t just helpful; it’s survival. A good budget doesn’t restrict your life; it gives you clarity, stability, and control. And when funds are limited, knowing exactly where your money goes becomes the key to reducing stress and avoiding financial mistakes that can snowball.

Whether you’re living paycheck to paycheck or want better control over your finances, here is a simple and effective way to create a budget and prioritize your spending.

The Starting Point

1. Start With Your Actual Numbers (Not Estimates)

Most people guess their income and expenses, and that’s why their budgets never work. You need to write down:

Exact monthly take-home income

All fixed expenses (rent/mortgage, utilities, insurance, car payment)

All variable expenses (food, gas, personal spending)

Tip: Pull the last 2–3 months of bank statements. This shows the truth of your spending patterns.

2. Separate Needs From Wants — Clearly and Honestly

When money is limited, clarity matters.

Needs (non-negotiable):

Housing

Utilities

Groceries

Transportation

Insurance

Minimum debt payments

Wants (optional or adjustable):

Eating out

Entertainment

Shopping

Subscriptions

Vacations

Upgrades

If a bill isn’t essential for living or maintaining safety, it belongs under wants.

This separation will guide all spending decisions going forward.

3. Use the “Priority Ladder” to Rank Your Spending

Think of your expenses like rungs on a ladder. The higher the rung, the more important it is.

Top Priority: Survival Expenses

These keep you fed, sheltered, insured, and able to work.

Middle Priority: Obligations

Debts, childcare, necessary repairs, and medical needs.

Lower Priority: Lifestyle Choices

Convenience, entertainment, subscriptions, upgrades.

Whenever money gets tight, spend from the top of the ladder downward.

Never from the bottom up.

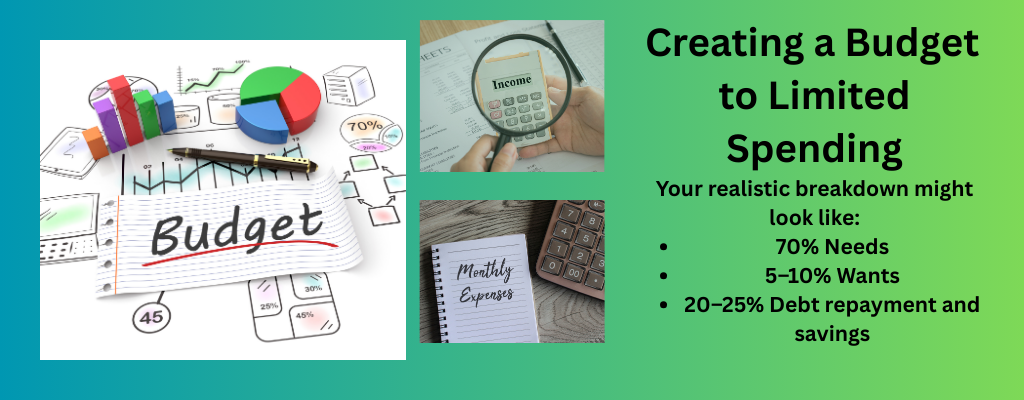

4. Create a Basic Budget Using the 50-30-20 Rule (Adjusted for Low Income)

If money is extremely limited, a traditional 50-30-20 budget doesn’t always fit. But we can adjust it.

Your realistic breakdown might look like:

70% Needs

5–10% Wants

20–25% Debt repayment and savings

If income is stretched thin:

Needs may be 80–90%

Wants may drop to 0–5% temporarily

Savings may be $10 a month — and that’s okay. Consistency matters more than the amount.

5. Cut Expenses Strategically — Not Emotionally

You don’t cut what makes you feel good; you cut what doesn’t provide value.

Examples of smart cuts:

Cancel unused subscriptions

Buy store brands instead of name brands

Cook at home 3 times more per week

Reduce streaming services to one

Renegotiate insurance or phone plans

Switch to cash envelopes for problem categories

High-impact cuts:

These changes give you more breathing room than trimming small items:

Refinancing or negotiating car insurance

Lowering internet or cable bills

Reducing restaurant spending

Cutting impulse purchases

You’ll be surprised how quickly small choices add up.

6. Build a Mini Emergency Fund — Even $100 Makes a Difference

Unexpected expenses hit harder when you have a limited income. Start small:

$10–$25 a week

Or save change from cash spending

Or put aside one small refund or gift

Your first goal: $100

Next: $500

Then: One month of expenses

Building slowly is better than never starting.

7. Track Your Spending in Real Time

A budget only works if you monitor it. Choose a method that fits your personality:

A simple notebook

An Excel sheet

A budgeting app

Cash envelopes for trouble categories

The key: Track every dollar as it is spent, not at the end of the month.

8. Give Your Money a Job Before You Spend It

This is a powerful concept known as zero-based budgeting. Before the month begins, assign every dollar a purpose:

Rent

Groceries

Gas

Savings

Debts

Spending

When every dollar has a job, you eliminate guesswork and overspending.

9. Revisit and Adjust Your Budget Monthly

Life changes. Bills go up. Needs shift. Income fluctuates. Review your budget:

What worked?

What went over?

What categories need adjusting?

Budgeting is not a one-time setup — it’s a monthly habit that strengthens your financial stability over time.

Final Thoughts: You Can Control Your Money, Even When It’s Limited

Budgeting isn’t about deprivation; it’s about direction.

It’s about taking control of the money you have instead of letting it control you.

When you know your priorities, track your spending, and give every dollar a purpose, your financial stress goes down, and your confidence goes up.

Remember that -Small steps build stability, stability builds freedom, and freedom starts with the budget you create today.